Comprehensive weather insights help safeguard your operations and drive confident decisions to make everyday mining operations as safe and efficient as possible.

Comprehensive weather insights help safeguard your operations and drive confident decisions to make everyday mining operations as safe and efficient as possible. Learn how to optimize operations with credible weather and environmental intelligence. From aviation safety to environmental compliance, our comprehensive suite of solutions delivers real-time insights, advanced forecasting, and precise monitoring capabilities.

Learn how to optimize operations with credible weather and environmental intelligence. From aviation safety to environmental compliance, our comprehensive suite of solutions delivers real-time insights, advanced forecasting, and precise monitoring capabilities. Net Import Turnabout

- Rebounding net imports of crude in EIA data resulted in the largest build to commercial crude stocks since the week ending June 5, despite refinery runs registering 863,000 bpd above week ending June 5 levels.

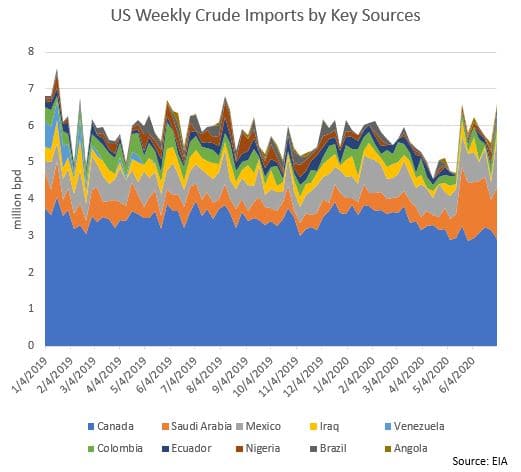

- EIA data for the week ending July 3 show US imports of Mexican crude oil jumping 106% from the prior 4-week average and 167% from the prior week.

- Even if crude stocks fall 24.0 million bbl in July as the STEO projects, this still leaves commercial stocks 17%, or 22 million bbl, above year-ago levels moving into August.

LOUISVILLE, KY. (DTN) — Last week in this report we discussed the much-needed narrowing of US net imports of crude. We detailed the importance of further declines in net imports in the coming weeks if we were to see the material draws to crude stocks needed to sustain the rally in crude prices. This week’s EIA report reinforced our view, as rebounding net imports of crude in EIA data revealed the largest build to commercial crude stocks since the week ending June 5, despite refinery runs registering 863,000 bpd above week-ending June 5 levels.

In contrast to futures price action last week, the WTI forward curve has moved to a greater degree of contango across all time spreads as this week has progressed. This highlights the struggle the US market has had in clearing both crude and product stocks, even amid peak seasonal driving season. Distillate fuel oil stocks continue to rise, even with exports less than 100,000 bpd below year-ago levels, refinery runs still 3.1 million bpd below year-ago levels, and refiners are working hard to maximize gasoline yield. This sends a clear message: the US economy is far weaker than stock market indices may lead some to believe.

Given the growth in COVID-19 case counts, hospitalizations and now once again deaths in the US, we expect domestic demand for crude and oil products to face headwinds in the coming weeks. It is for this reason that we emphasize global demand for US crude and products; as demand for US exports are critical if inventory levels are to be brought back within historical ranges.

Crude Imports

The EIA reported crude imports surging 1.4 million bpd in the week ending July 3. At 7.4 million bpd, imports were reported at their strongest weekly pace since peak demand season last August. So why the reported strength in imports when stocks are already brimming, and the forward curve is not incentivizing further storage?

EIA data show that the surge in crude imports last week came from widespread strength in deliveries from most of the top US suppliers of medium and heavy sour crude, excluding Canada. With Canadian crude imports trending lower as a narrow WCS-WTI spread continues to disincentivize crude-by-rail imports, US refiners are turning to Latin America for stronger supplies of heavier sour crudes.

EIA data for the week ending July 3 show US imports of Mexican crude oil jumping 106% from the prior 4-week average and 167% from the prior week. Imports of Mexican crude were pegged at 1.33 million bpd, up 834,000 bpd from the prior week. This was the strongest week of imports from Mexico in EIA records since February 2012. Imports from Brazil and Colombia were also reported pushing higher on the week.

Additionally, the EIA reported imports of Saudi Arabian crude surprisingly jumping to their highest since the week ending June 5. This appears to be the final push of Saudi arrivals that followed from the Saudi price cuts early this spring and may even reflect the EIA reporting imports that had already made landfall in prior weeks but were not counted by the EIA due to delays in bills of lading. Regardless, at 1.4 million bpd, imports of Saudi crude were up 595,000 bpd on the week in EIA data. The weekly pace of imports of Saudi crude were up nearly 3-fold year-on-year. Imports of Iraqi crude, meanwhile, are down 52% from year-ago levels at just 174,000 bpd.

We expect US refiners to cut crude import volumes in July while increasingly turning to short haul cargoes of heavier sour crudes from Latin America as volumes from Saudi Arabia and typical OPEC suppliers fall off amid coordinated output and export cuts.

Crude Exports and the Adjustment Factor

US crude exports were reported falling 705,000 bpd in the week ending July 3. At just below 2.4 million bpd, exports were their weakest since the week ending November 1, 2019. This sent net imports of crude surging just over 2.1 million bpd last week. As a result, net imports were reported at 5.0 million bpd – their strongest since early last August amid peak refinery runs and summer driving demand.

As we discussed last week, ship tracking firm Tanker Trackers reported US crude exports of nearly 3.8 million bpd during the week ending June 26 – roughly 700,000 bpd above the EIA’s figure for the week. The EIA’s own data suggested that they may have underestimated exports during the period. The EIA’s adjustment factor, which has in recent months largely reflected the EIA overestimating crude production, jumped higher in last week’s report. After narrowing for three consecutive weeks and falling to just -52,000 bpd in the week ending June 19, the adjustment factor rebounded to -631,000 bpd in the week ending June 26. In the week ending July 3, Tanker Trackers saw US exports average nearly 1.1 million bpd above the EIA’s reported figure, at 3.5 million bpd. With what looks to be the EIA sizably underestimating actual exports once again last week, the adjustment factor moved into greater negative territory, coming in at -765,000 bpd.

Stronger exports of crude are largely dependent on continued Chinese buying interest in the coming weeks. As we had projected, the wave of VLCC arrivals bringing crude to the US has led to a rebound in back haul cargoes to China. It is likely that Chinese buyers took advantage of falling VLCC shipping rates in late June and booked additional US cargoes for loading in the coming weeks. But a lack of VLCC deliveries to the US could lead to a shortage of the vessels needed to sustain stronger exports to Asia as we move through August and into September, unless shipping rates fall further or imports from the Arab Gulf rebound.

Net Import Outlook

U.S. net imports of crude have averaged 3.9 million bpd over the past four report weeks in EIA data. The latest Short-Term Energy Outlook from the EIA reported June net imports of crude nearly 400,000 bpd below what their weekly estimates reported. That said, we do agree with the EIA’s outlook for net imports of crude in July.

The STEO calls for net imports of crude to drop to an average just below 2.5 million bpd in July. If crude oil inputs at US refiners rise to an average 14.85 million bpd as forecast, this is expected to lead to a draw to commercial crude stocks of 24.0 million bbl during the month.

Looking out further, one of the most important projections in the EIA’s July STEO report was their call for an extreme rebound in net imports of crude from August forward. The EIA forecasts net imports of crude rebounding nearly 1.0 million bpd in August from July and nearly doubling between July and December. After dropping to 2.44 million bpd in April of this year, the EIA projects net imports will surge to 5.23 million bpd by April of next year. This scenario assumes a normalization of US demand while domestic crude production slides steadily lower.

Conclusion

Even if crude stocks fall 24.0 million bbl in July as the STEO projects, this still leaves commercial stocks 17%, or 22 million bbl, above year-ago levels moving into August. And let’s not forget the 23 million bbl of commercial crude recently pushed into the strategic reserve. As such, we continue to expect WTI to face major resistance at the $44 level if we see prices push higher later this month as stocks draw down.

With distillate fuel oil stocks and demand in the US still reflecting the prolonged spread of COVID-19 across the nation, we remain hesitant to believe that US refinery runs are going to rise to just 2.9% below year-ago levels by October as the EIA projects in their STEO. Strength in net exports of refined products and weakness in net imports of crude remain crucial for the sustained draws to stocks needed to push crude prices higher in the coming days.